Small and Medium Enterprises (SMEs) are the bedrock of the Nigerian economy, yet access to affordable credit remains a major hurdle for many entrepreneurs. The Central Bank of Nigeria (CBN), through various intervention programmes, aims to bridge this gap by providing loans at lower interest rates with longer repayment windows. However, a significant challenge persists: historically, only a small fraction of the total intervention financing has reached smaller businesses.

For entrepreneurs who have felt the struggle of turning an idea into reality, the journey often feels impossible with commercial banks demanding collateral they do not have or documentation they cannot afford. This comprehensive guide cuts through the confusion, providing a realistic, step-by-step overview of how to access CBN-backed loans in 2026, what to expect, and the pitfalls to avoid.

2026 Intervention Programmes: What’s Currently Available?

The CBN does not disburse loans directly to businesses. Instead, it works through participating financial institutions, including commercial banks and microfinance banks (MFBs), to channel funds to specific sectors of the economy. While the list of programmes can change, several key schemes remain cornerstones of the intervention strategy.

The Micro, Small and Medium Enterprises Development Fund (MSMEDF) is designed to promote financial inclusion by providing affordable loans to small businesses, especially those led by women and youth. The Agribusiness/Small and Medium Enterprise Investment Scheme (AGSMEIS) targets agricultural and SMEs across various sectors, with loans disbursed through participating banks. For those in the creative industry, the Creative Industry Financing Initiative (CIFI) focuses on areas like fashion, ICT, media, and entertainment.

Two other significant programmes are the Targeted Credit Facility (TCF), originally launched to support businesses during economic disruptions, and the Nigeria Youth Investment Fund (NYIF), which channels capital to youth-owned businesses at lower interest rates.

It’s important to note that these programmes run in batches and may be replaced with new structures. Therefore, always confirm the active status of any scheme at the official CBN website or through your participating financial institution before starting the application process.

Step-by-Step Guide to Accessing CBN Intervention Loans

Accessing these funds requires preparation and a clear understanding of the process. Here is a realistic breakdown of what you need to do to make yourself eligible for intervention funding in 2026.

Step 1: Formalise Your Business with CAC

Before you can even think of applying, your business must be a recognised legal entity. This means registering your business with the Corporate Affairs Commission (CAC). Many SMEs operate informally using personal accounts, which is a huge barrier because lenders need to see a structured business entity with proper records. In addition to your CAC certificate, you must obtain a Tax Identification Number (TIN) for the business and open a dedicated business bank account.

Step 2: Prepare Strong Financial Records

CBN intervention loans are meant for growth, not for emergencies. Banks and partner institutions want to see that you can repay. This means you need to have proper bookkeeping that shows revenue and expenses, bank statements for your business account, and cash flow projections. If you cannot afford audited accounts, at least have well-maintained records. Businesses that rely on informal financial habits will struggle to qualify, even if they have great products or services.

Step 3: Connect with Participating Financial Institutions

As mentioned, CBN intervention funds are usually disbursed through partner banks, microfinance banks, or development finance institutions like Bank of Industry (BOI). The quality of your engagement with these institutions matters. Visit multiple institutions, talk to relationship officers, ask about the intervention programmes they participate in, and request guidance on documentation. Your goal is to find the institution whose requirements and programme focus align best with your business needs.

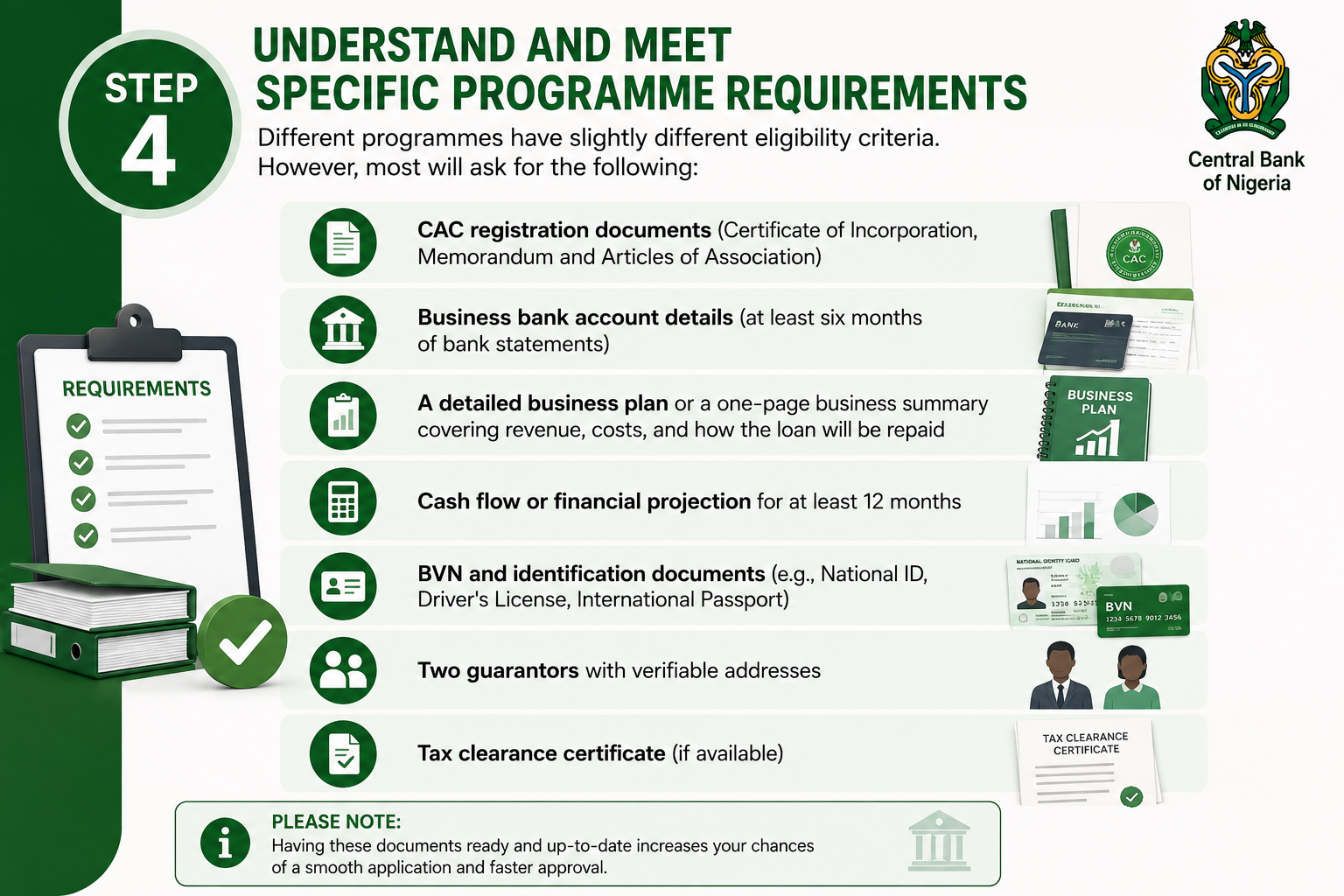

Step 4: Understand and Meet Specific Programme Requirements

Different programmes have slightly different eligibility criteria. However, most will ask for the following:

- CAC registration documents (Certificate of Incorporation, Memorandum and Articles of Association)

- Business bank account details (at least six months of bank statements)

- A detailed business plan or a one-page business summary covering revenue, costs, and how the loan will be repaid

- Cash flow or financial projection for at least 12 months

- BVN and identification documents (e.g., National ID, Driver’s License, International Passport)

- Two guarantors with verifiable addresses

- Tax clearance certificate (if available)

Being prepared is non-negotiable. Missing one document can delay your application by weeks or lead to an outright rejection.

Step 5: Submit a Complete Application Early

Unlike regular bank loans where you might negotiate in person, intervention funds often run on batch applications. Submitting early, accurately, and completely increases your chances of being considered for the next funding batch. The sooner you get your documentation in order and engage with the PFI, the better your position. And do not panic if approvals take time; it is common, but early preparation and follow-up help more than late-stage scrambling.

Understanding the 2026 Banking Environment

The banking sector in Nigeria is undergoing significant changes, which directly impact how banks assess loan applications. Following the March 31, 2026, recapitalization deadline, banks are now required to have a significantly higher minimum capital base. This has two effects: banks have a higher lending capacity, but the Capital Adequacy Ratio (CAR) has also been tightened, meaning banks are more likely to offer fixed-rate loans to stable businesses to avoid risk.

A key driver for SME lending in 2026 is the Loan-to-Deposit Ratio (LDR) mandate. The CBN requires banks to lend at least 65% of their deposits to the ‘Real Sector’ (manufacturing, agriculture, and SMEs). Banks that fail to meet this target face penalties. This essentially forces banks to look for credit-worthy businesses to fund. If your compliance profile—including your Tax Clearance Certificate and NIN/BVN linkage—is in order, you are exactly the kind of borrower banks are now hunting for.

Critical Pitfalls and Tips for Success

Navigating the loan application process requires vigilance. Here are some critical points to keep in mind.

- Define a Clear Purpose: Lenders price risk based on clarity of purpose. “Stock for the December trading season” is fundable. “Business expansion” is not.

- Run a Credit Check on Yourself: Pull your credit report from CRC, CreditRegistry, or FirstCentral before any lender does. Address any errors before they are used against you.

- Read the Offer Letter Line by Line: Pay attention to the total repayable amount, repayment schedule, default consequences, prepayment terms, security clauses, and any cross-default with other facilities.

- Set Up Automated Repayment: Standing orders or direct debit reduce the risk of missed payments far more reliably than calendar reminders.

- Beware of Scams: Phishing of women borrowers via WhatsApp impersonation is a documented pattern. Ensure you are communicating with official bank channels.

Leave a Reply